Quick answer: how much do forgotten subscriptions cost?

A single forgotten $10/month subscription costs $120/year. A $15/month subscription costs $180/year. Two or three forgotten subscriptions can quietly become $300–500/year, especially when annual renewals and price increases are included.

The average person pays between $300 and $500 a year for subscriptions they no longer use. Not subscriptions they might cancel. Subscriptions they haven't opened in months and didn't remember they had.

That's a gym membership that became a monthly donation to a company you forgot about. A streaming service you bought for one show and never cancelled. A free trial that converted three months ago and has been billing $9.99 ever since.

The money isn't the worst part. The worst part is that you don't even notice it leaving.

The math you're probably getting wrong

Ask someone how much they spend on subscriptions each month, then walk through their bank statement with them. The gap between what they think they pay and what they actually pay is usually 30–60%.

Three things cause this gap:

Free trial conversions. You tried the AI photo editor, forgot about it, and it turned into $12/month. Most trials convert silently — no confirmation, no receipt that stands out, just a line on your card statement that says something vague like "PAYPAL *PHOTOAPP."

Price increases you missed. Spotify went up. YouTube Premium went up. Your cloud storage doubled. The emails landed in your Updates folder and you never read them. The first time you notice is when someone asks you to check.

Subscriptions you share. Your partner pays for Netflix, you pay for HBO, your family plan includes Apple Music. You only see half the picture on your own statement, so you never see the real total.

Run the math yourself: take your guess, then open your last two bank statements and add up every recurring charge. The difference is what you're losing without knowing it.

Why you don't catch them on your own

Your bank isn't built to show you subscriptions. It's built to show you transactions. The difference matters.

A bank statement shows Spotify the same way it shows a coffee and a parking ticket — as a timestamp and an amount. It doesn't group recurring charges. It doesn't tell you what's about to renew. It doesn't show you that the same service charged you $9.99 in January and $12.99 in April because of a price increase.

The reminder cycle works against you too. Subscriptions renew at different times of the month — one on the 3rd, another on the 15th, another on the 28th. Each individual charge is small enough to ignore. Together they're significant, but you never see them together.

This is why people discover forgotten subscriptions during tax season or when they switch banks — the forced review exposes what the monthly rhythm hides.

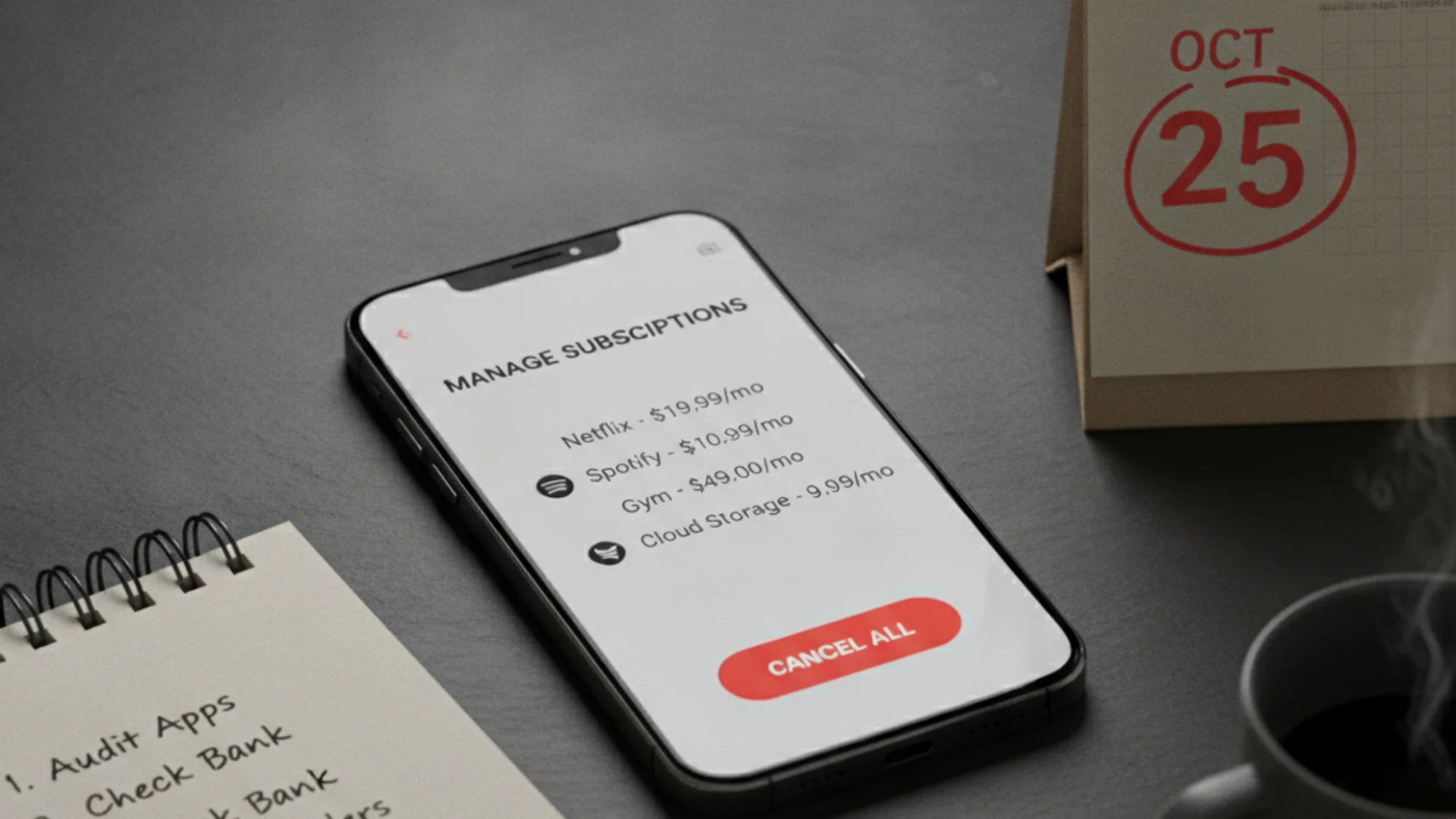

The subscriptions people forget most

Based on what users find when they first start tracking, these are the most commonly forgotten:

- Free trials that converted — especially AI tools and productivity apps with 7-day trials

- Annual subscriptions — they charge once, you forget about them for 11 months, then they hit again

- Phone apps — App Store and Google Play subscriptions are hidden in a separate menu, not on your bank statement

- Cloud storage and backups — you signed up when your phone warned you about space, then never thought about it again

- Second streaming accounts — the one for your kid's tablet, the one you share with your ex, the one you bought for a flight in 2024

One real example: a Subnesio user found they were paying for two separate iCloud storage plans — one through Apple, one through their carrier. They had set up the carrier one three years ago and forgotten it existed.

The annualised math of one forgotten charge

The single most useful exercise is multiplying a small recurring charge by twelve.

- $4.99/month → $59.88/year.

- $9.99/month → $119.88/year.

- $14.99/month → $179.88/year.

- $19.99/month → $239.88/year.

- $59/year billed once → $59 every January until cancelled.

Two of the $9.99 charges plus a $14.99 you forgot about is $420 over twelve months — for services you may not have opened in three. That is roughly the C+R Research perception gap of $133 a month, $1,596 a year, that the average US consumer underestimates their subscription bill by.

Annual subscriptions amplify the effect. A yearly tool feels free for eleven months and then bills again. If the renewal slips past your review window, you have prepaid for another year of something you might not have re-bought today.

Why people miss the charges

The cost only happens because the charges hide. Three structural reasons forgotten subscriptions accumulate:

- Free trials that converted silently — no confirmation, just a line item three months later.

- Annual plans billed once a year — out of sight for eleven months.

- Cards you don't routinely audit — App Store and Google Play subs, partner's card, prepaid balances.

- Price increases — Spotify, Netflix, YouTube Premium have all raised prices in 2024–2026 without anyone explicitly agreeing to the new price.

- Bank trackers that match against known merchants only — indie creators, regional services, and bundled charges slip through the tag list.

What this looks like over a year

Pick a realistic forgotten basket:

- One $9.99 streaming service used twice → $119.88.

- One $14.99 AI tool you stopped opening → $179.88.

- One $69 annual cloud backup auto-renewed → $69.

- One $4.99 phone app from a 2024 install → $59.88.

Total: $428.64. None of these individual charges is large enough to trigger attention. Together they are most of a flight, a month of groceries, or a year of a different service you would actually use.

For the next step — finding and stopping these charges — see how to cancel subscriptions you forgot about. For why your bank app is not catching them on its own, why your bank subscription tracker is not enough. For the full picture of what people actually spend, average monthly subscription spending in 2026. For the trial conversion specifically, free trials that auto-charge on day 7.

If catching these charges before they renew is the part that fails by hand, Subnesio is one option — see Subnesio pricing.